How to Stop Living Paycheck to Paycheck: 9 Tips & Tricks

Published on: 11/07/2022

With nearly two-thirds of the U.S. population living paycheck to paycheck according to a study conducted by LendingClub Corporation many Americans find themselves constantly battling financial stressors. If you are one of them, check out these nine strategies to help you stop living paycheck to paycheck.[1]

1. Understand where your money goes, then create a budget

Creating and sticking to a budget can help anyone regardless of their financial health. But if you’re stuck living in the paycheck-to-paycheck cycle, learning how to create a budget can go a long way towards helping you gain control of your finances. Budgets help you track your expenses to get a clearer picture of where your monthly income goes and where you can cut back.

While you can choose from a number of budgeting methods, the 50/30/20 rule can be a good place to start. The rule allocates money into three separate buckets based on your take-home pay: 50% for mandatory expenses like housing, food and utilities, 30% for wants like subscription services and treats and 20% for savings and debts like student loans. While the 50/30/20 suggestion may prove unrealistic for certain financial situations, many financial advisors recommend it as a good place to start.

[2]

What budget categories should you include?

No matter what budgeting method you choose, break down your spending into categories. This initial step helps you identify areas where you spend too much money and shift some of the money you save to other categories.. In either case, a budget gives you a snapshot of your current financial situation and may even help you figure out how much of your paycheck to save.

Essential budget categories include the following:

- Rent or mortgage

- Utilities

- Food

- Transportation

- Insurance

- Healthcare

These categories make up the typical essential expenses, but you may have others depending on your unique situation. After the necessities are accounted for, you can budget in plans for your discretionary income, such as hobbies, gym memberships and gifts. If you need help starting a budget, check out these budgeting challenges to try this year.

2. Look for other income opportunities

If you’ve completed your budget and discovered you simply need more money coming in, look into opportunities to increase your income. A traditional part-time job may be an option, but you might also consider starting a side hustle or monetizing a hobby. You can sell things you make on Etsy or let go of unneeded items on Offerup. Other ways to make extra cash include grocery delivery with Instacart and picking up a freelance gig on Upwork. Spend some time researching different companies and platforms so that you understand the ins and outs of these companies. That way, you can see if any fit your unique circumstances before jumping in and getting started.

3. Make a plan for debt repayment

Even if you have your current monthly expenses under control, previously accumulated debt — such as credit card debt or personal loans — can hang over you like a cloud. Prioritizing debt repayment can help you save money in the long run, allowing you to put money towards your other expenses rather than interest payments. Depending on your personal preferences, you can choose from several methods to get out of debt.

Try the debt snowball method

The debt snowball method prioritizes paying debts down from the smallest to the largest, regardless of interest rate. This method tends to work best for people who enjoy the immediate reward of getting a quick win and checking items off their to-do lists.[3]

Try the debt avalanche method

If you want to save as much money as possible, you may prefer the avalanche method of debt repayment. With this method, you pay off the debt with the highest APR first, working your way through the debts in order of interest rate.[3]

4. Plan for unexpected expenses

Just when you think you’ve established a manageable budget, your car breaks down or your refrigerator goes on the fritz. That’s why it is important to have funds for unexpected expenses.

Consider starting an emergency or sinking fund

Both types of funds have you saving money each month but with different goals:

Sinking fund: A savings account with a specific purpose — that’s a sinking fund in a nutshell. Whether you want to buy a car or take a vacation, a sinking fund helps you reach your savings goals by earmarking money for a specific purchase with a defined timeline.[4]

Emergency fund: An emergency fund, on the other hand, helps you prepare for the unexpected. While you don’t know what emergency will occur or when it may strike, it makes sense to put money aside as a safety net. To calculate an emergency fund goal, think about how much money you can reasonably save and how much your typical emergency expenses have cost in the past.[5] Experts typically recommend three to six months’ worth of expenses, but anything is a good start.

While you may not be able to save for both simultaneously, make it your goal to start with an emergency fund. Once you feel comfortable with your emergency fund, you can start your sinking fund for other purchases.

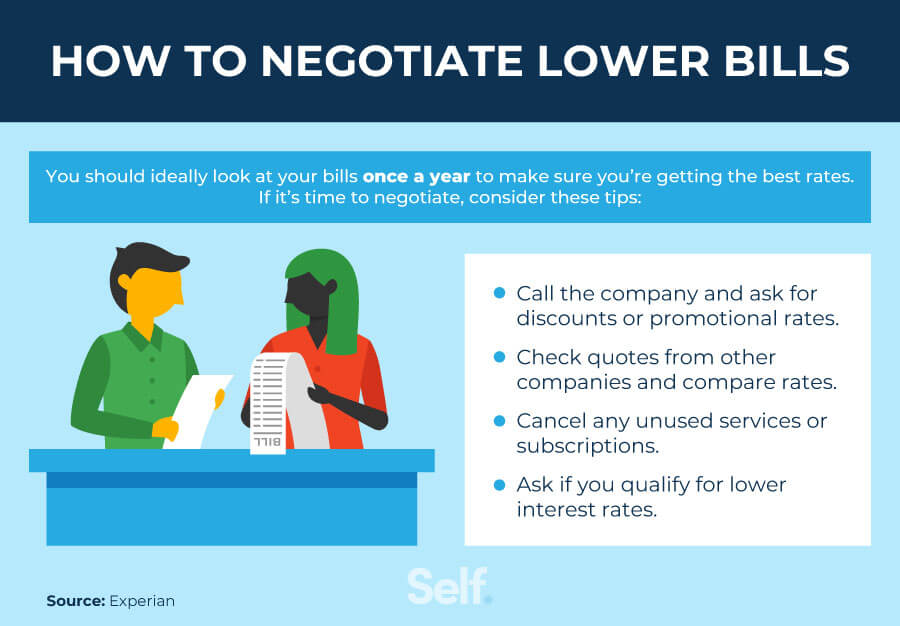

5. Try to negotiate lower bills

While some bills are non negotiable, others may leave room to negotiate a lower price, better interest rate, early termination or a more favorable payment plan. In some cases, you can directly contact a company representative to see what your options are for lowering your bills. In other cases, you will negotiate with yourself by taking a look at your bills and deciding which services you can downgrade or eliminate entirely.[6]

This list helps you get started:

- Memberships: You may find it impossible to get out of some membership contracts, but some companies might be willing to work with you — either by offering you a more basic plan or giving you a discount for paying annually instead of monthly. Think about trying this with your gym memberships, association memberships and even Amazon Prime, which currently offers a discounted yearly rate.

- Utilities: Some people are lucky enough to live in an area with multiple service providers. If you’re one of them, you may be able to shop around to negotiate a better deal on your energy bills. Some may also offer rebates if you install energy-saving devices or reduce your energy use during peak times.

- Internet: Having multiple options to choose from can also help you lower your internet bill. Even if you don’t have a choice in providers, you may be able to get more bang for your buck by getting more channels, bundling services or downgrading your plan to save money.

- Cell phone: Reduce your cell phone costs by looking into bundling services or changing providers.

- Insurance: Make sure you’re getting the best deal on your car insurance rates by shopping around and re-evaluating your options regularly. If you buy a new car, move, or change your driving habits, you may find that you can lower your auto insurance premiums. Some insurance companies also offer discounts for safe drivers, paying all at once or, in some states, having a good credit score. If your emergency fund can handle it in the case of an accident, raising your deductible often lowers your rates.

- Interest rates: Talk to your credit card companies. You may be able to negotiate a lower interest rate, get a late charge reversed or simply downgrade a card with an expensive annual fee.

6. Limit excess spending

Sometimes we think of our routines as necessities. If you take a fresh look at your spending habits, however, you may find that you can save a significant amount of money. While it may seem challenging at first, try to create some new (less-expensive) habits. For example, make food at home or try thrift-store shopping. For a good place to start, check out these easy money saving challenges you can try right now.

7. Avoid taking on more debt

Until you get a handle on your current spending, try to avoid taking on more debt. While you may feel tempted to spend money that you don’t have — and still won’t have next month when the bill comes due — remember that your long-term goal is to stop living paycheck to paycheck. The less new debt you take on, the faster you can achieve that goal.

8. Create a financial roadmap

True financial freedom begins with a financial plan. Any financial roadmap should include an examination of your spending, a solid budget and both short-term and long-term financial goals.

Short-term goals:

- Do a full audit of all spending and cancel anything unwanted. Practice good financial hygiene by getting rid of any subscriptions or memberships you don’t use.

- Stick to a budget to manage your money. Your budget should help you distinguish needs from wants. The next step is sticking to it and prioritizing necessities as much as possible. If you feel deprived of your splurges, remember that this is a short-term goal — you make sacrifices today to achieve financial freedom tomorrow.

- Get a copy of your credit report. Take advantage of your free annual credit report by visiting annualcreditreport.com. Keep track of what is reported and take the time to look carefully for inaccuracies that could be impacting your score.

- Commit to starting small with monthly savings. Even a little savings can be a big relief in the event of smaller unexpected expenses such as repairing your cell phone or paying for minor car repairs.

Long-term goals:

- Work toward becoming debt free. Of course your budget needs to address your living expenses and other necessities, but it should also include steps to pay down your debt.

- Find higher-paying employment. If your income simply doesn’t cover your monthly expenses (or enable you to meet your financial goals), consider seeking a more lucrative job. While it requires more work upfront, you may find it more than worth the effort when your new paycheck starts rolling in.

- Plan for retirement. When you’re living paycheck to paycheck, retirement may be the last thing on your mind. But to protect your future self, any financial plan should include at least some steps towards this long-term goal.

- Minimize credit card usage over time. Credit cards can provide a constant temptation to spend more money than you have. For that reason, limiting your reliance on credit cards can help you live within your means.

9. Take advantage of free resources

When you feel buried under a mountain of expenses, it may seem that everything costs money. But whether you want to find better employment or educate yourself on personal finances, a variety of free resources can help you achieve your financial goals.

Consumer Financial Protection Bureau

The Consumer Financial Protection Bureau (CFPB) offers adult financial education tools and resources. With worksheets, handouts, audio recordings and other tools, the CFPB hub addresses such topics as money management, debt collection and bank accounts. The dozens of free PDFs available on the website include “Take control of your auto loan,” “Understand your credit report,” and “How to stop mystery credit card fees.”

[7]

National Credit Union Administration

An independent federal agency, the National Credit Union Administration (NCUA) works to raise consumer awareness and increase access to credit union services. The NCUA’s Financial Literacy & Education Resource Center aims to help people make smarter financial decisions by promoting financial literacy. Some of the many tools and resources available on their website include mortgage loan calculators, videos on payday loans and tips for preventing identity theft.[8]

Purdue OWL resume workshop

If your financial plan involves seeking better employment (or a second job), you may want to check out the resume writing tips from the Purdue Online Writing Lab (OWL). Topics include resume sections, resume design, scannable resumes and even resumes for military veterans. Other ways to polish your job application package include taking their job skills inventory, viewing sample cover letters and learning how to tailor employment documents to specific audiences.[9]

CareerOneStop Employment Recovery

Sponsored by the U.S. Department of Labor, CareerOneStop’s Employment Recovery website provides resources on unemployment and jobs. Whether you’re looking to get back to work, find a job immediately or explore a new potential career, CareerOneStop can help you get started. Resources include a job search tool, interest assessments, self-employment tips and links to free and low-cost training options.[10]

Stay positive on your financial journey

You may hope for an instant solution to your money problems, but financial freedom is a marathon, not a sprint. Improving your financial health takes time and planning. Most importantly, try not to get overwhelmed. Taking proactive steps and focusing on the positive can go a long way towards curbing financial anxiety.

If building your credit plays a role in your financial plan, check out the tools Self offers to put you on the right path for building credit. For other ideas, the Self Personal Finance blog offers tips on everything from budgeting to insurance to help you structure your finances to avoid living paycheck to paycheck.

Sources

- Cision PR Newswire. “2/3 of the U.S. Population Now Lives Paycheck to Paycheck,” https://www.prnewswire.com/news-releases/23-of-the-us-population-now-lives-paycheck-to-paycheck-301536811.html. Accessed July 2, 2022.

- Forbes. “Your Guide To The 50/30/20 Budgeting Rule,” https://www.forbes.com/advisor/banking/guide-to-50-30-20-budget/. Accessed July 2, 2022.

- CNBC. “What’s the difference between the ‘snowball’ and the ‘avalanche’ debt repayment methods?” https://www.cnbc.com/select/debt-snowball-vs-debt-avalanche/. Accessed July 2, 2022.

- Next Advisor, “A Sinking Fund Can Help You Save For a Big-Ticket Splurge. Here’s How To Start One.” https://time.com/nextadvisor/banking/sinking-fund/. Accessed July 2, 2022.

- Consumer Financial Protection Bureau. “An essential guide to building an emergency fund,” https://www.consumerfinance.gov/an-essential-guide-to-building-an-emergency-fund/. Accessed July 2, 2022.

- Experian. “How Often Should You Negotiate Your Bills?” https://www.experian.com/blogs/ask-experian/how-often-to-negotiate-bills/. Accessed July 2, 2022.

- Consumer Financial Protection Bureau. “Tools and resources to use with the people you serve,” https://www.consumerfinance.gov/consumer-tools/educator-tools/adult-financial-education/tools-and-resources/. Accessed July 2, 2022.

- National Credit Union Administration, “Financial Literacy & Education Resource Center,” https://www.ncua.gov/consumers/financial-literacy-resources. Accessed July 2, 2022.

- Purdue University. “Purdue Online Writing Lab,” https://owl.purdue.edu/owl/job_search_writing/resumes_and_vitas/introduction.html. Accessed July 2, 2022.

- U.S. Department of Labor, CareerOneStop. “Employment Recovery,” https://www.careeronestop.org/EmploymentRecovery/default.aspx. Accessed July 2, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).